As securities finance moves to blockchain rails, "onchain repo" is becoming a headline feature, and the largest lending protocols are positioning around it. The trouble is that most of what gets called repo onchain is not repo. It is variable-rate margin lending against securities collateral, which is a different instrument with a different risk profile.

The distinction matters, because the thing that makes repo useful to institutions is exactly the thing the variable-rate version strips out.

What repo actually is

A repurchase agreement is a sale of a security with an agreement to buy it back at a set price on a set date. In practice it is short-dated secured borrowing: the holder of a high-quality asset, usually a Treasury, hands it over as collateral, takes cash, and repays at a fixed rate on a fixed date to reclaim it. The rate is locked for the term. The maturity is defined. Both sides know the full economics at the moment the trade is struck.

That is not incidental detail. It is the definition. A repo without a fixed rate and a fixed term is not a repo, the same way a bond without a coupon and a maturity is not a bond. The fixed rate is what lets the borrower fund a position at a known cost. The fixed term is what lets both sides match the financing to the life of the trade. Strip either out and you have a different product. (On why those two properties are independent, see fixed term vs fixed rate.)

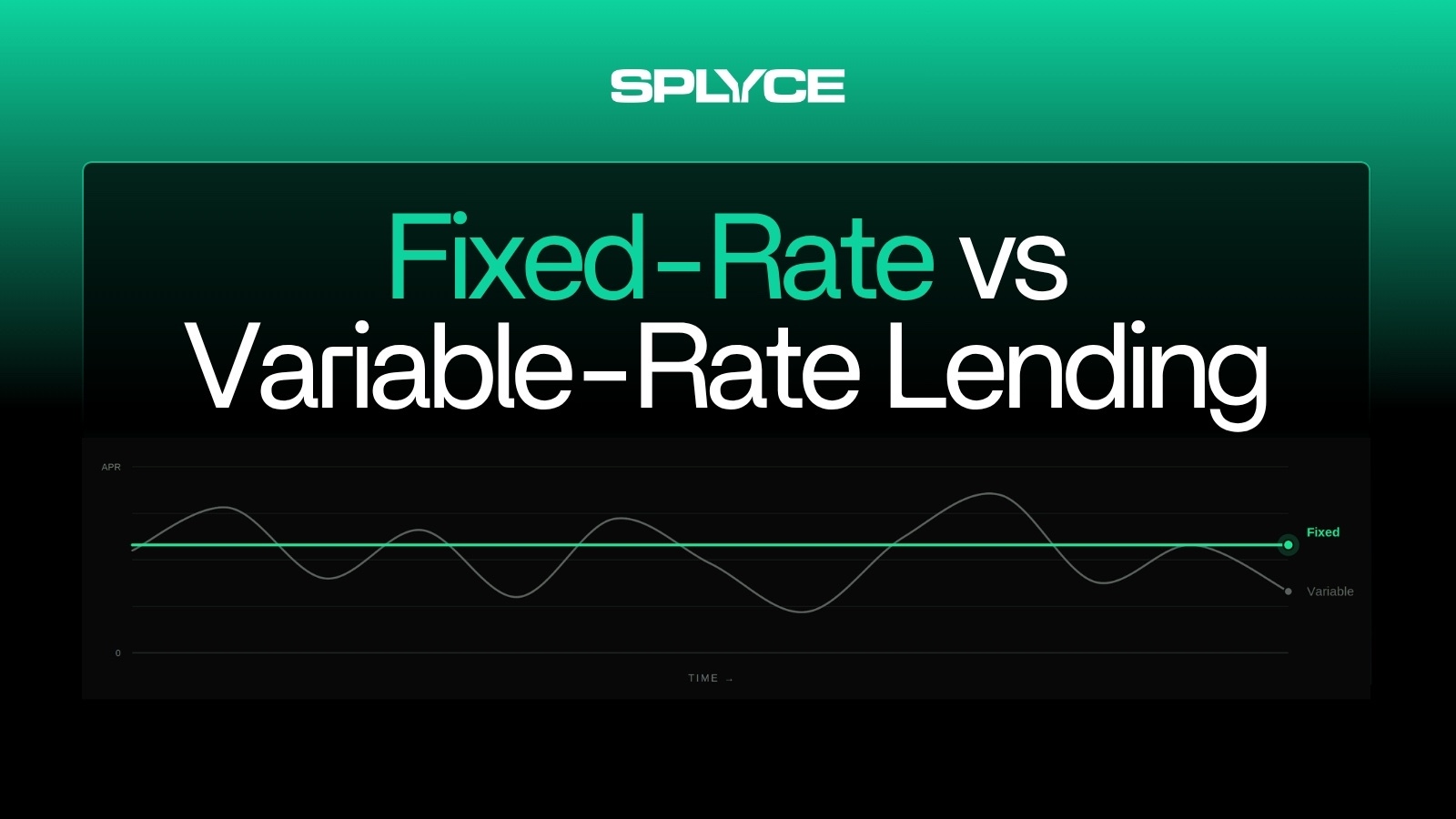

What "onchain repo" usually means today

Most onchain versions work like this: a tokenized Treasury is posted into a pooled lending market, and the holder borrows a stablecoin against it at a rate set algorithmically by pool utilization. The rate floats. The position is open-ended, callable on demand. There is no maturity.

That is a useful instrument. It is also a margin loan, not a repo. The borrower does not know the cost of capital for the life of the facility, because the rate reprices continuously. Calling it repo borrows the credibility of a $12 trillion-a-day market for a product that does not share its defining feature. (For the rate mechanics, see fixed-rate vs variable-rate lending.)

The utilization trap

The deeper problem with the variable-rate model is not just that the rate moves. It is how it moves, and what moves it.

In a pooled market, the borrow rate is a function of utilization, how much of the available liquidity is currently lent out. Below an optimal point, rates rise gently. Above it, the curve is built to go nearly vertical, spiking the rate to force new deposits in or push borrowers out. This is a deliberate balancing mechanism, and in calm conditions it works.

The consequence is that a borrower's cost of capital is set by other people's behavior, not their own. A few large lenders withdrawing, or a surge in borrow demand, can push utilization past the kink and double or triple the rate in hours, with nothing the borrower did to cause it. You can be a responsible borrower, well inside your collateral limits, and be repriced into distress by a liquidity event you had no part in.

It is also self-reinforcing under stress. A rate spike makes leveraged positions uneconomic, forcing borrowers to unwind. Unwinding consumes liquidity and pushes utilization higher, which spikes the rate further, which forces more unwinds. The mechanism is most violent precisely when conditions are worst, which is exactly when an institution needs its funding cost to be stable. Recent events on the largest variable-rate venues made this concrete: utilization spiked, borrow rates went vertical, and positions nowhere near their liquidation thresholds were forced to unwind by financing cost alone.

For a margin trader, that is a bad day. For an institution running a financed book, it is disqualifying. No treasurer can operate against a cost of capital that another participant's exit can triple overnight.

Why this rules out the variable-rate model for real repo

Repo is the largest short-term funding market in the world because of the certainty fixed rate and fixed term provide. A dealer finances inventory knowing the exact carry. A fund borrows against its Treasuries at a cost it can model to the dollar. That certainty is not a nicety; it is the product. A financing instrument whose cost can be reset by other participants is not the instrument repo desks have relied on for decades.

There is a second problem on the collateral side. Pooled, oracle-priced, continuously-liquidated lending works for liquid Treasuries that can be marked and sold every second. It breaks against collateral that cannot: tokenized private credit, receivables, anything with a redemption cycle measured in days rather than blocks. There is no live price to margin against and no liquid market to liquidate into. The instruments that most need term financing are the ones the variable-rate model serves worst.

What onchain repo should be

Real onchain repo keeps the two properties that define it. The rate is fixed at origination. The term is fixed to a maturity. The loan settles on a known date rather than floating indefinitely, and resolution is scheduled rather than triggered by a price feed. Because the rate is locked for the term, no other participant's behavior can change the borrower's cost once the trade is struck. For liquid collateral, a venue can layer oracle-based margining on top if it wants it. For illiquid or restricted collateral, it runs oracle-free, with resolution at maturity and a designated counterparty to settle positions that need an intermediary, the onchain equivalent of the collateral-disposal function repo desks have always relied on.

This is the structure Splyce is built around: fixed-rate, fixed-term lending against tokenized real-world assets, with the certainty that makes repo repo preserved rather than abstracted away.

The securities-finance market is genuinely moving onchain, and that is the right direction. But the value of repo was never the word. It was the locked rate and the defined term. A market that keeps those delivers what institutions actually use repo for. One that drops them is something else, however it is labeled.