The phrases sound interchangeable, but they describe different things. Splyce combines both in fixed-rate, fixed-term lending against tokenized real-world assets, so it is worth separating exactly what each one locks.

What a fixed rate locks

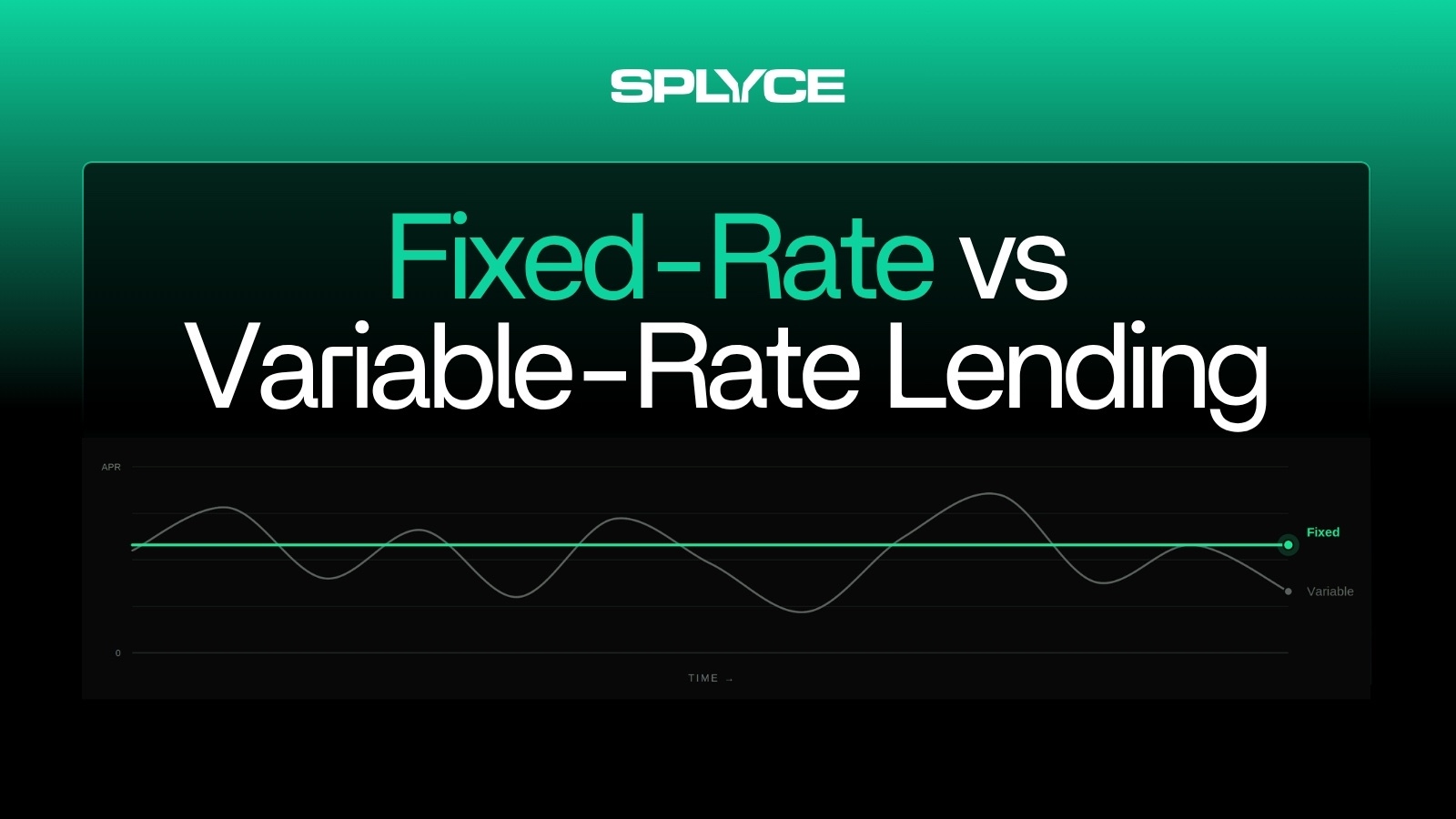

A fixed rate fixes the price of the loan, the interest rate. Once set, it does not move with utilization, demand, or market conditions. The opposite is a variable rate, which floats, as covered in fixed-rate vs variable-rate lending.

What a fixed term locks

A fixed term fixes the duration, the maturity date when principal and interest settle. The opposite is open-ended, or perpetual, lending: you can withdraw at any time, but the position never matures. Concretely: a 30-day Single Asset Vault is fixed-term, settling on a known date, while a USDC deposit in an Aave pool is open-term, withdrawable any block but never reaching a maturity.

Why the two are independent

Because they lock different things, a loan can mix them in four ways:

- Variable rate, open term: the typical DeFi money market, such as Aave or Compound. Withdraw anytime, rate floats.

- Fixed rate, open term: the rate is pinned but there is no maturity. Uncommon, because a fixed rate with no maturity leaves the lender carrying duration risk with no term commitment to offset it, so it rarely exists as a designed product.

- Variable rate, fixed term: a dated loan whose rate still moves during its life, like a floating-rate note in traditional finance.

- Fixed rate, fixed term: both locked. This is the structure of traditional fixed-income credit, and the one Splyce Single Asset Vaults bring onchain against tokenized real-world assets.

Most onchain lending is the first combination. Institutional credit is the last.

How Splyce combines both

Single Asset Vaults are fixed-rate and fixed-term: the rate locks at deposit and the loan settles at a defined maturity, a 30-day maximum at launch, expanding as the book grows. An institutional lender is asking two questions before committing capital, what rate they earn and when they get it back, and a SAV answers both before a dollar moves.

For RWAs the pairing is not cosmetic. The fixed rate gives the borrower a cost of capital it can actually underwrite. The fixed term does something separate: it matches the loan's maturity to when the collateral can realistically be redeemed or resolved, so the position never has to be force-closed mid-term against an illiquid asset. This is also why the pairing fits real-world assets better than volatile crypto: a tokenized Treasury holds its value to a known redemption, so a term loan against it is straightforward, where the same structure against a volatile asset would have to price a full term of potential downside into the rate. One property solves the pricing problem, the other solves the collateral-matching problem, and together they are the heart of fixed-rate RWA lending.

A fixed rate answers "what do I earn?" A fixed term answers "when do I get it back?" Institutional credit needs both locked, and that is exactly what a Single Asset Vault does.