Fixed-rate, fixed-term lending against tokenized real-world assets is the model institutions can actually underwrite. To see why, it helps to compare the two ways a lending rate can behave.

How variable-rate lending works

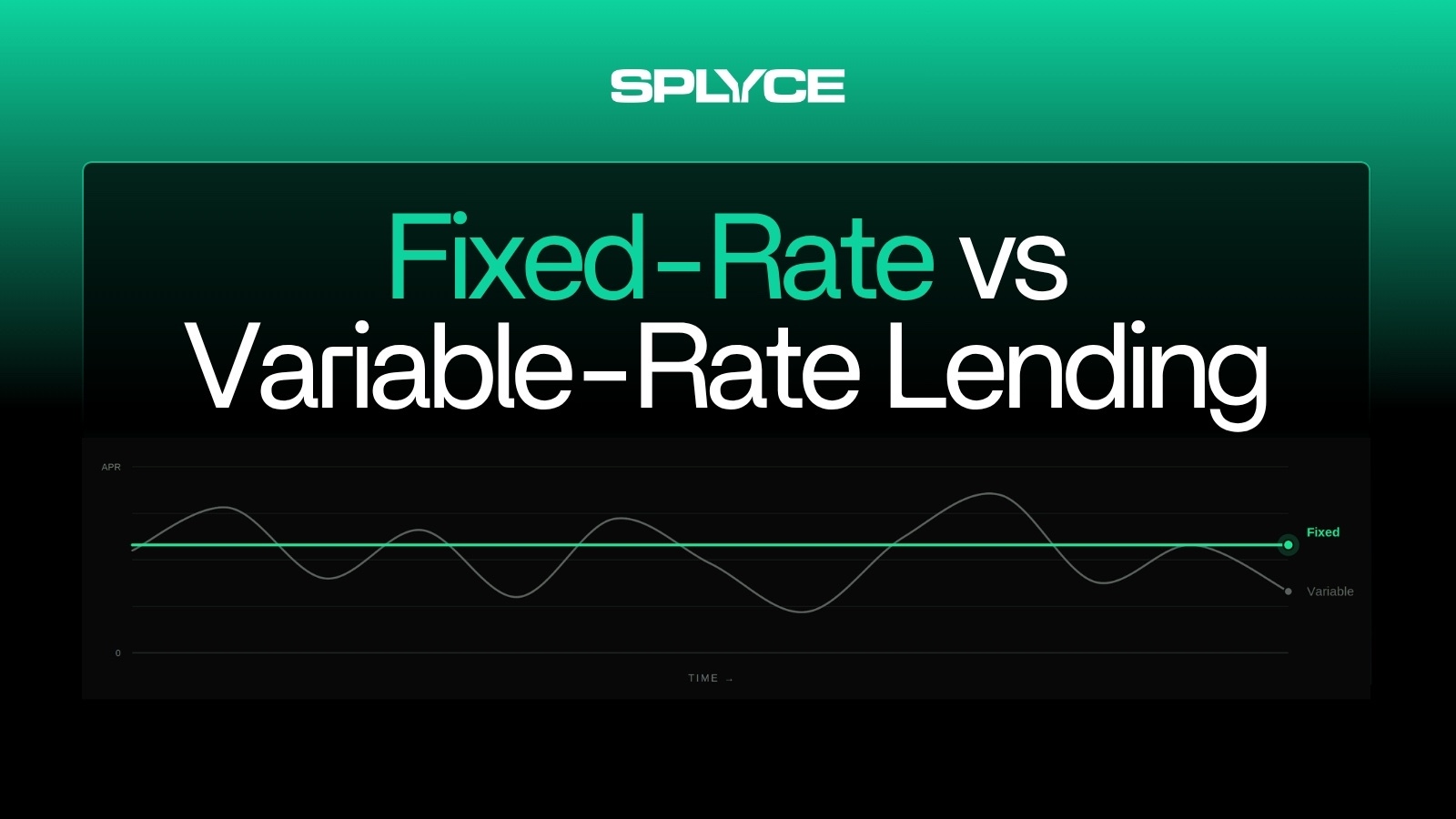

Money markets like Aave and most Morpho markets set rates algorithmically from utilization. When borrowing demand rises, rates rise; when it falls, rates fall. Deposits are open-ended and withdrawable on demand, which suits liquid crypto collateral well. But the yield you see today is not the yield you will earn tomorrow, and the rate can move sharply in either direction before your position closes.

How fixed-rate lending works

A fixed-rate loan sets the interest rate once, at origination, and holds it for the full term. Both sides know the exact economics in advance. The tradeoff is commitment: capital is typically locked until maturity. On why that maturity is a separate property, see fixed term vs fixed rate.

A worked comparison

Put $500k to work two ways for 30 days. In a Single Asset Vault backed by tokenized Treasuries at a fixed 9% annualized, you know on day one that you will earn about $3,700, settled at maturity, whatever rates do in between. In a floating Aave USDC market, the same $500k might start at 6%, climb to 12% as utilization spikes, or fall to 3% if borrowers leave. Over the month you could earn more than the vault or less, and you will not know which until it is over.

The variable market gives you liquidity and the chance of a higher print. The vault gives you a number you can underwrite. A trader chasing the best available rate may prefer the first; a treasurer financing a balance sheet almost always needs the second.

Why fixed rates matter for RWAs

Real-world-asset borrowers are institutions, and institutions do not scale on variable-rate debt, because the cost of capital has to be known. That is why every serious attempt to bring institutional credit onchain, from Notional's fCash to Term Finance to Morpho's fixed-rate markets, is converging on fixed, term-based rates. Splyce Single Asset Vaults apply the same structure to tokenized real-world-asset collateral, with the rate locked at deposit and, for RWA collateral, oracle-free by default, so there is no price feed forcing a mid-term liquidation.

There is a deeper reason variable rates fail here, beyond uncertainty. Variable-rate pools also let lenders withdraw on demand. That works for liquid crypto that can be sold in minutes, but against term-locked RWA collateral it is the exact setup that produces runs: callable money on one side, illiquid collateral on the other. Matching a fixed term on the lending side to the collateral's own settlement profile removes that mismatch.

Borrowers feel the same pull. An institution financing inventory or settlement cannot run its book against a rate that reprices every block; a fixed rate for a fixed term is what lets it plan. That alignment, lenders who want a knowable yield and borrowers who need a knowable cost, is what makes fixed-rate markets stick for institutional credit where variable ones never did.

A lender does not have to choose

For a lender, the two models are not either/or. If you want fixed-rate RWA exposure without locking capital for a full term, splyceUSDC gives you passive access to the same credit. It is a yield-bearing token deployed mostly across the SAV book, with a short-duration liquidity sleeve held for redemptions. Its yield floats as a blended rate rather than being fixed, because it spreads across many vaults and maturities at once, and it stays redeemable from that liquidity sleeve, with a queue under stress when redemptions run ahead of it.

Variable rates give liquidity and a shot at a higher print. Fixed rates give a number you can underwrite. For credit against real-world assets, the number wins. See fixed-rate RWA lending for the full model.